So you’ve got a great business idea and you want to create a WordPress startup. Maybe you’re developing a web app, a developer shop, design agency, or a pageview monster that generates AdSense revenue. Regardless, if you’re a first-timer, you’re bound to have lots of questions bouncing around in your head.

The title of this post refers to The Art of the Start. I read it back in 2004 shortly after graduating from my undergrad program, and it answered many of the questions I had at the time. You may have the same questions now, but a lot has changed since then, so consider this an updated cheat sheet version.

Before we begin, please don’t consider any of the following to be legal advice. These are my own observations and experiences starting a WordPress business. You should consult an attorney for your specific situation.

What I’ll be covering in this guide:

- Starting a Company

- Riches in Niches

- Assessing Your Finances

- Pricing Your Product or Service

- Defining Your Brand

- Building Your Website

- Streamlining with Business Tools

- Promoting Your Business

- Closing a Sale

Starting a Company

You should first educate yourself on the types of company formations available in your home country. Here in the U.S., the main options are sole proprietor, LLC, LLP, S-Corp, and C-Corp.

Then there is the tax aspect to consider. For example, you can be a single-member LLC but file as an S-Corp for tax purposes. Sounds confusing, right?

In general, if you’re looking to raise capital down the line or you anticipate being acquired, then a C-Corp is the common approach.

Or if you’re starting a web agency, for example, and don’t intend to raise capital or be acquired (at least not for quite some time), you’ll probably want to have your attorney explain the advantages/disadvantages of going with an LLC, LLP, or S-Corp.

If you’re a freelancer, going the single-member LLC route is probably the most common approach. It requires minimal paperwork and filing fees, plus it keeps your taxes relatively simple. You’ll file what’s called a “Schedule C,” and you can even file your tax return via something like TurboTax Home & Business.

If you plan to have partners and don’t want to be liable for their conduct, consider the LLP approach. It’s commonly used for partnerships composed of doctors, architects, lawyers, or accountants.

An S-Corp is more formal and has more compliance obligations than an LLC, such as creating a board of directors, annual reports, and shareholder meetings, whereas an LLC is pretty informal and the requirements are minimal. Another striking difference is that with an LLC, profit/loss can be allocated disproportionately among owners.

With an S-Corp, profit/loss are assigned to each shareholder based on shares of ownership. One main advantage of an S-Corp over an LLC is that if you do decide/need to convert to a C-Corp at a later date, it can be done much faster and more easily. Converting an LLC to a C-Corp can involve lots of headaches, time, and expense.

Do I Need a Lawyer?

Yes. Talk to a legal expert and get advice. It is absolutely worth the money if you are serious about starting your own business. Laws vary by state and country; getting an expert opinion will help you navigate the business laws and regulations relevant to you.

Do I Need a Business Plan?

Probably not. You’re better off spending your time developing your product, recruiting a team, and raising seed money if you need it. It’s next to impossible to get a bank loan, and banks are the only places left that ask for a long-winded 30-page business plan these days.

If you’re planning on pitching angels and VCs, start researching how to create an awesome pitch deck. I, of course, am strictly anti-VC but I understand that not everybody is…

Do I Need to Raise Capital?

It depends on your personal preference and the type of business you’re starting. If someone tells you “never raise capital,” they’re an idiot. Try starting an electric car company or something like Amazon without capital and see how that goes.

Obviously, some types of businesses absolutely require raising funding while others do not. If you’re starting a web agency or a business that requires little money to get off the ground, then you’re better off retaining 100% ownership and running things the way you like. However, if you’re going into a field where scaling quickly makes sense to avoid being squashed like a cockroach, then consider getting your pitching shoes polished.

Do I Need a Co-Founder?

Many studies have shown your odds of success are higher when you have a co-founder. Most incubators and startup accelerators actually prefer you have one, but it’s not required.

Ideally, you want a co-founder who has a complementary skill set. Apple was successful because Jobs and Wozniak were perfect complements to one another. Each was strong where the other was weak.

In addition, working as a team can be fun and it’s easier to get through the low points when you are sharing them with someone else. Would you rather stay up all night alone cranking out pitch decks or do that with someone by your side?

Make sure you don’t mind being married, figuratively (or literally, in my case), to your co-founder. You’ll be spending a lot of time with them and if you don’t jive personally, neither of you will have much fun.

Do I Need to Hire People?

Absolutely. Dave McClure, who started 500 Startups, is famous for saying the best founding team consists of a hacker, hustler, and a designer. At the very least, you’re going to need:

1. Developers

You might be thinking, “I’m a business guy/gal, can’t I just hire a developer on Upwork to build my app?” Typically, the best developers aren’t on Upwork. You want to hire developers who you can offer equity to so they have a vested interest in your company (and in keeping their job) and will put their heart and soul into their work.

2. Salespeople

As the founder, you’re going to be selling all the time. Whether it’s to potential customers, potential employees, or potential investors. You absolutely need to hire people skilled in sales if you want to scale up properly.

3. Designers

How many sites have you stumbled upon and thought, “Wow, they have great features but this UI makes me want to puke.” Probably more than a handful. So get designers on board so your UI looks amazing.

Hiring and Retaining Great People

Studies have routinely shown that emotional intelligence is the most important predictor of career success—more than any other single factor. Prior to this finding, researchers scratched their heads at the fact that average-IQ people would outperform those with the highest IQs a whopping 70% of the time.

Why does this matter? Because emotional intelligence (EQ) is critical to being a good boss. You need to understand what motivates your employees and act accordingly.

But what happens if you aren’t a good boss? Well, your employees will leave. There’s a good chance your employees are getting job offers all the time without your knowledge. If you don’t treat your employees like gold they’ll be gone.

Retraining is expensive and time-consuming, so you want to avoid that as much as possible. Turnover is also a surefire way to kill morale.

Riches in Niches

Here’s a lesson I learned a long time ago: greedy eyes are bad for your wallet.

One of the best scenes from any movie is from 1987’s Wall Street. Gordon Gekko gives a ridiculous speech to Teldar Paper shareholders about how greed is good. Gekko makes some valid points; however, the fact is that greed isn’t good.

What type of greed are we talking about? The “be all things to all people” greed. The “we have to sell to all types of customers” greed.

You see, most founders and companies want to serve the entire market—capture the “whole pie,” so to speak. Sounds like a good approach, right? I mean, the more potential customers, the more potential revenue, and so on.

The problem with this approach is that, over time, other companies will specialize in various sectors of the market and chip away at your customer base, and it’ll be almost impossible to compete with them.

If you’re working on a product that serves ten types of customers and their product serves only one of those, their focus will give them a huge advantage.

Finding your niche

Focus is key, but what is the best approach to finding your niche? Find one within your space that isn’t currently occupied and use it to scale up quickly.

Even though the potential market size of your slice might not be as large as the whole pie, you’ll find supply/demand more in your favor. Once you’ve dominated your niche and reached decent scale, you can consider going into other verticals and adding more products specialized for those markets.

If you’re worried your niche is too small, consider this: Mark Cuban once invested in a guy who draws cats for a living. If there are riches in cat drawings, you might be surprised what you might find in your niche.

Assessing Your Finances

Let’s be honest: If you’re starting broke with no cash to invest in your company, you definitely have it harder than someone with money. But that doesn’t mean you can’t create a valuable company. You’ll just need to be more creative, and it might take longer to get your company off the ground.

Talk to an Accountant

With the money that you do have, talk to a professional about any and all financial questions related to starting and running your business. Also, ask about what tax benefits are available to you as a business owner.

Raising Capital

At this point, you might be thinking, “Shouldn’t I just raise money from an angel or VC?” If you’re not well-connected to the local financing community and don’t have traction (e.g. revenue or explosive user counts), you should probably focus on getting some momentum before going this route.

Why? Because the best way to get in touch with a real angel or VC is to be referred to them, rather than cold calling or emailing them. They get so many pitches that this will help you cut through the clutter.

So that leaves asking friends and family to raise capital. I personally find it awkward to pitch friends and family but some people don’t, and if your friends and family happen to be wealthy, even better.

Here are some other ways to get capital together:

- Sell your time. Ever wonder why so many first-time founders start an agency or service business? Because it requires little capital. Building a product-based business often requires far more capital. A service business is relatively cheap to set up and it can often give you the seed money to start your product-based business.

- Credit cards. I’m not advocating for running up tons of credit card debt, but some companies have been successfully financed this way. If you’re going to pursue this route, first get your credit in order with a service like Credit Karma. This way, if you take out any credit cards you’ll get better interest rates and limits on them.

- Small business loans. Full-size Small Business Administration (SBA) loans that are available in the U.S. might be hard to get if you’re just starting out, so first focus on their microloan program.

- Peer-to-peer lending. If you can’t get a microloan from the SBA, then see what kind of loans and rates you can get at places like Funding Circle, LendingClub, Prosper, and OnDeck.

- Partner up. If you have a great idea and bring value to the table, then consider partnering with someone who has the cash to co-found the company. Yes, they’ll get more equity because they’ll be making more of a “capital contribution,” but that’s life.

Pricing Your Product or Service

There are a few approaches often discussed that you can take when it comes to determining your pricing. But first, here’s what I recommend you don’t do:

- Mistake #1: Going with your gut. You’ll typically over- or undervalue your product one way or another, selling yourself short. How can you sell yourself short if you overvalue/price your product? We’ll get to that in a minute.

- Mistake #2: Following the competition. Looking at your competition and pricing your product or service accordingly will likely fall short as well. Why? Because the perceived value of your product to potential customers is based on a number of factors. You are likely not a perfect clone of your closest competitor, so you will each be able to extract different prices even if your products are very similar.

Where does that leave us with pricing? Economic theory. Specifically, price elasticity of demand, which is the measure of responsiveness of the quantity demanded for a good/service to a change in its price.

If you’re thinking, “Urgh… what?” Basically, we want to find what’s called optimal pricing, which means finding the price that maximizes your revenue.

Step 1: Estimate the Price Elasticity of Your Product or Service

We want to figure out how sensitive your customers are to price changes in your product. At one end of the spectrum, you have products with high elasticity, meaning consumers are very sensitive to price changes. At the other end, you have products with low elasticity, sometimes referred to as inelastic.

Let’s look at an example for each end of the spectrum, keeping in mind that most products fall somewhere in between:

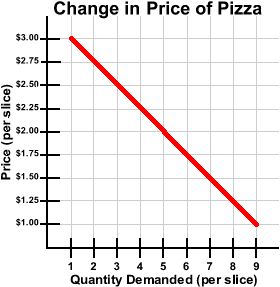

Example #1: Pizza

Pizza is considered very elastic, meaning if you jack up the price you’ll sell a lot less. Here’s what the graph of price elasticity looks like for a slice of pizza. Notice the angle of the line is about 45 degrees.

So if the pizza shop owner tries to charge $3 per slice, they’ll only sell one slice, so revenue is $3. If they only charge $1, they’ll sell nine slices and revenue will be $9. But neither of those prices maximizes revenue.

In this case, the optimum price is between $1.50 and $1.75 a slice. Both yield the highest overall revenue at $10.50. (Seven slices sold at $1.50 provides the same revenue as six slices sold at $1.75.)

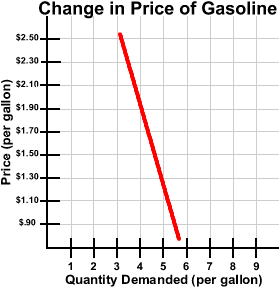

Example #2: Gasoline

Gasoline, on the other hand, is considered inelastic, meaning that even if you jack up the price you’ll sell almost the same amount. That’s because people still need it. Here’s what the graph of price elasticity looks like for a gallon of gas. Notice the line is much steeper here.

Notice that if the station owner charges $1.10 per gallon, they’re going to sell a little over five gallons. If they jack it up to $1.90 (nearly double), they’re still going to sell four gallons.

Now look back at the pizza graph above and think about what happens to that poor soul if they try the same trick. Their demand plummets and they sell way less. That’s why sales of things like gasoline and medications remain fairly steady in a recession, whereas non-essentials like spa services and expensive restaurants watch their sales tank.

Do people need your product or service?

Now that you understand how price elasticity works, you can probably estimate on which side of the spectrum your product or service falls. Do people absolutely need it? Will a change in price have much effect on the number of units you sell?

Step 2: Do Some Real-World Testing

Once your website is up and running (we’ll get to that soon) run some A/B tests with a tool like Optimizely to figure out which type of landing page works best, given whatever prices you have set initially.

If you’re going to experiment with different price points to see which one maximizes revenue, you need to try to make sure you’re only playing with one variable at a time (in this case price). As you test various price points on your landing page, make sure you are keeping all else constant in your business as much as possible.

This means no layout or design changes while testing, no pursuit of major press coverage, and no fiddling with your AdWords budget and bidding. Ideally, you want to isolate as much as possible. Otherwise, you’ll be confusing correlation with causation.

Maximizing Your Revenue

Your aim should be to make your product or service as inelastic as possible so your customers will be unable to live without it, allowing you to charge more without killing demand. Google and Apple have done this by creating entire ecosystems that revolve around their products.

If you’re running a SaaS, offer different plans at different price points that appeal to a variety of users. If Pagely only had one plan, we’d probably see a dip in signups.

How many plans do you need? Most WordPress startups tend to go with a number between two and five, depending on the industry. Figure out how many customer personas you have and then create a corresponding plan for each one.

Defining Your Brand

Branding encompasses all of the ways you establish an image of your company in your customers’ eyes. This can include company names, logos, icons, symbols, taglines, and even design.

A lot of newbie entrepreneurs suck at branding and it’s not their fault. It took me a while to truly understand its power, and I had it hammered into my head in B-school for four years in undergrad. Here’s how you can tell that someone doesn’t get branding:

- Terrible company name

- Shoddy website design

- Logo looks like it was made for $10

- Products/features aren’t named in a memorable way

- Domain name is terrible

- Little to no usage of trademarks, whether ™ or ®

Take a look at your own WordPress startup and be honest. Are you checking all the boxes? Have you created a real brand or just a pile of garbage?

When someone mentions a well-known brand, expectations and experiences usually come to mind. McDonald’s? Fast, unhealthy food. Apple? Quality, reliability, premium, expensive. Walmart? Low prices, long lines, zero people to help you find anything. Google? Engineering, scale, intelligence. WordPress? Open-source, free, scalable, ubiquitous, flexible.

Think long and hard about what you want your WordPress startup’s brand to convey and make sure your company name, tagline, logo, and design reflect that.

You’ll also want to come up with a marketing plan and strategy, making advertising just one piece of it. Give your brand the smell test above and see how you measure up. Then try to figure out how to reverse engineer Coca-Cola’s branding. I’m still working on that myself.

Building Your Website

If you haven’t already, you’ll need to launch a website for your WordPress startup. Since we’re talking about how to create a WordPress startup here, it makes sense that you would want to build your website using WordPress.

I won’t go into detail about building a site with WordPress. You can read about that in our guide to enterprise website development. Instead, I want to talk about scaling and why hosting infrastructure is critical to your company’s success.

Don’t End Up Like Achilles

In Greek mythology, when Achilles was a baby it was predicted that he would die young. To prevent his death, his mother Thetis took him to a river named Styx, which offered powers of invulnerability and dipped his body into the water.

But because she held Achilles by his heel, it was never washed over by the magical waters. Achilles grew up to be a warrior who survived lots of great battles. However, one day a poisonous arrow lodged into his heel, killing him swiftly.

Many WordPress startups are just like Achilles in the sense that they have everything going for them but have a major weakness: their hosting architecture and ability to scale. In fact, it still happens all the time, despite the many startups that have popped up to address the issue.

Why You Need Scalable Managed WordPress Hosting

You’d think WordPress startup founders would worry about the scalability of their product or service and the infrastructure powering it, but so many skip over this critical step. You’re excited to launch and hosting seems boring, or you’re focused on your product and customers.

But have you ever built a really popular application with more than a million users? If the answer is “no” then you likely need to slow down for a minute and think long and hard about how well your setup will scale. Don’t let startup excitement and euphoria cloud your judgment.

This is where working with a managed WordPress host like Pagely can help. You’re probably not an expert in web hosting, and you probably don’t have an engineer to optimize your server or fight off cyber attacks. Tending the back end of your site requires time and technical expertise. When you partner with a Managed WordPress Hosting solution, we’ll manage your site’s uptime, security, performance, and more.

Streamlining with Business Tools

Running a company is by no means an easy task, but there are a lot of tools and apps that can make your life easier. A few years ago, I did an interview with Matt Medeiros (now, Pagely’s own superstar) for his show Matt Report, during which I talked about many of the tools I use and thought might help other people who are launching WordPress startups.

Here are some of the tools I mentioned along with other personal recommendations:

Accounting

If you’re just starting out then you definitely need an accounting system of sorts. Previously, QuickBooks was the de facto choice, but nowadays there are many others, most of which are easier to use.

If you plan on creating an S-Corp or C-Corp, then you should definitely check out Xero, which is neat in that it can help you find an accountant in your geographic region who is trained in their system and can be linked as the accountant on your profile.

Benefits and Payroll

Gusto is both affordable and intuitive for first-time users. Y-Combinator-backed Zenefits is another great option. These can help you with managing health insurance, 1099s, worker’s comp, retirement plan administration, and more. In addition, they can help with more HR-type stuff like tracking paid time off, employee onboarding/offboarding, I9s, and more.

Billing

If you’re planning on doing recurring billing at scale, then I recommend checking out Recurly. It’s great for collecting granular data on your subscriptions, like how long the average customer on a plan sticks around or how many invoices went initially uncollected last month.

Recurly will also ensure you have nice, pretty data to show in the event you need to raise capital or get acquired. No VC or diligence team wants to spend their time combing through your own homegrown billing system’s data or, worse, having to run calculations to figure out things you should have been tracking in the first place.

If you plan to sell or products or services in person, then I highly recommend getting a Square reader. And if you need to cut those all-important invoices and you’re not in a subscription-based Recurly plan, then get set up with Freshbooks and enter invoicing nirvana.

Conference Calls

No, Skype is not a good solution if you’re going to be talking with serious business people. There are infinite things that can go wrong and you’ll look like a cheapskate trying to talk to the CIO of XYZ who thinks that Skype is for calling your grandma in Florida. So get set up with UberConference or Zoom and start making legit conference calls.

Cost-Per-Click

If you’re going to be managing serious CPC campaigns in Google Ads, I highly recommend downloading the latest copy of Google Ads Editor. This powerful software runs locally on your laptop/desktop and lets you make changes at scale with ease. Need to adjust 1000 ads at once in various ways? Done. Need to quickly scan 1000 ad groups? Done.

If you want to get nice, pretty monthly or quarterly reports on your AdWords campaigns (among other things), then check out Raven Tools. If you’re running an agency of sorts you can white label their stuff and your clients will think you’re a genius.

CRM

Getting a CRM is one of the most important things you can do to increase your closing/tracking of inbound leads. Here at Pagely we use Close.io, which is run by a really nice guy named Steli Efti who personally helped us come on board. They also have an API you can do cool stuff with.

G Suite. It’s the only logical choice, in my mind. Yes, they got rid of their awesome free plans, but their service is well worth the $5/mo. per user. And keep in mind one “user” can have multiple email aliases, so the pricing is even better than it sounds. Think of a user as a mailbox and an alias as an address.

Email Marketing

You’re going to be building a mailing list, right? I think Mailchimp or ActiveCampaign are great options.

Legal

If you’re looking to pursue a trademark, I recommend starting with a search on Trademarkia. From there you can decide whether to use their services or hire an independent IP attorney. Each has its advantages and disadvantages.

LegalZoom and Rocket Lawyer are other resources but, much like Trademarkia, just know that they should be considered a resource and not the resource.

If you plan to have contracts or documents signed, then you’ll probably want to check out places like DocuSign, Adobe Sign, and HelloSign.

Motivation

If you’re feeling overwhelmed or down in the dumps, then hop over to either Matt Report or Mixergy (or better yet, both) to get some inspiration. Watching videos is more fun than reading books, and you’ll often learn things that founders wouldn’t reveal in print form since it’s off-the-cuff.

Both Matt and Andrew do a great job; each caters to a specific type of audience, with Matt focused more on the WordPress side and Andrew on the general startup space. You’re better off watching ten different hour-long founder stories via video than spending ten hours with one founder’s book.

Office Space

Unless you’re going to be meeting clients on a daily basis or absolutely need space for your team to work beyond your local co-working space, renting an office isn’t typically necessary during the beginning phase.

If you need to meet with current or potential clients, get yourself a Regus Businessworld membership so you can rent their Class-A conference rooms on the fly. You’ll have the same view and location as those on other floors spending thousands per month with long-term leases, and you’ll just be paying for the room by the hour and be on your way when you’re done, client impressed and contract in hand.

Retirement

If you’re planning on flying solo and never hiring employees, then I highly recommend looking into Fidelity, as they are one of the few that allow you to run a SEP IRA as well as a Solo 401K. I won’t get into the details of the tax advantages that allows, but let’s just say that having both in your arsenal maximizes the amount you can put away and minimizes your tax liability.

I say “flying solo” because the Solo 401K is designed for companies without employees, otherwise, you’d need a general 401K and have to comply with ERISA rules that sound scary.

SEO

If you need to find all the broken links on your site (and who doesn’t) then you should check out Integrity if you’re running a Mac. It is a simple, free program and does just that. Those of you on Windows should check out Xenu’s Link Sleuth, which does the same thing.

If you want to go a little more advanced with spidering tools, download a free copy of Screaming Frog SEO Spider, which has a few extra bells and whistles. If you want to reliably track your organic rankings, something like Authority Labs would be an excellent choice.

For a comprehensive guide, take a look at The 2019 SEO Checklist for Webmasters.

Social Media

If you’re going to be managing a bunch of social media profiles (and you probably will be), then you’ll want some way to reliably blast your message out to all three or four of them at once. The cheaper option would be something like HootSuite, and a more polished option would be something like Sprout Social.

Support

Maybe not the sexiest of tools, but one you’ll probably be spending a fair amount of time with. At Pagely we run Zendesk while others swear by Freshdesk. To each their own.

Promoting Your Business

“How much should I spend on marketing?”

I’m often asked this question because I’ve started a few companies that have done between hundreds of thousands and millions in annual revenue, which doesn’t make me too cool for school, it just means there’s a chance I know what I’m talking about.

Surprisingly, it’s not just first-time founders who ask me — even seasoned entrepreneurs still don’t have a gauge for what their competitors and those in their industry are spending on marketing (and advertising), or even what they should be allocating to help promote their brand.

Many are jaded. They say “advertising doesn’t work,” or “advertising is for big companies with big budgets,” or perhaps aren’t patient enough to allow the proper time for ROI to kick in.

Do you think GEICO saw an immediate return when they started running those TV ads? Do people really whip out their laptop or tablet and start getting car insurance quotes while watching TV? Maybe now more than before due to the second screen trend, but most people see the commercial and continue on about their day.

But what’s the first brand that comes to mind when you think of car insurance? If you’re like me, it’s GEICO. They’ve got great “mind share,” and when people like me do get a car insurance quote, we typically check GEICO — and maybe even check them first.

One last anti-marketing comment you’ve likely heard from blowhards is something along the lines of “just make a great product like Apple and you won’t have to spend anything on marketing.” That is a pile of nonsense. Despite Apple making great products, they still spend a ton of money on marketing. In 2015, they spent a whopping $1.8 billion on advertising. Yep, and that puts them among the top spenders overall.

So let’s take a look at what you need to know about marketing.

How Much Should I Spend on Marketing?

The first thing to understand is that you shouldn’t be asking “what amount,” but rather “what percentage.”

First of all, hopefully your company is growing if you’re thinking about ramping up marketing spend, so using a static amount is suboptimal. Second, it’s much easier to compare and benchmark yourself against other companies both in your specific industry and in business in general when you talk in percentages.

What Big Companies Are Spending on Marketing

It’s important to understand what large companies spend on marketing for a few reasons. First, you might be competing with them directly or indirectly, so it gives you a snapshot of your competition and comprises one aspect of competitive research.

Second, since data on your WordPress startup competitors is often hard to get (e.g., you likely aren’t publishing what you spend on marketing, either), knowing the percentage that large companies spend will at least give you some idea in the event you can’t dig up much on the startups in your vertical.

The 2017 CMO Survey found that the mean (average) marketing budget as a percentage of revenue/sales was 7.9%. When broken down by industry, we get even more interesting findings:

- Banking/Finance/Insurance = 9.2%

- Communications Media = 9.0%

- Consumer Packaged Goods (think P&G) = 9.1%

- Consumer Services = 18.9%

- Education = 12.0%

- Energy = 8.3%

- Healthcare = 9.0%

- Manufacturing = 2.4%

- Mining & Construction = 3.0%

- Service Consulting = 7.5%

- Retail/Wholesale = 4.4%

- Tech/Software/Biotech = 9.7%

- Transportation = 8.5%

I’ve emphasized the “tech/software” and “service consulting” categories above since they’re probably the most applicable to launching a WordPress startup. Notice that even consulting businesses, which tend to rely on referrals, still spend more than 5% of revenue. Also, note that tech/software firms have the third-highest spend at 9.7%.

What Small Companies and Startups Are Spending on Marketing

The Small Business Administration suggests the following guidelines for small businesses setting their marketing budget:

- 2–3% for run-rate marketing

- 3–5% for startup marketing

They note that the above should be adjusted for the industry your business is in, its current size, and phase of growth. Remember that industry data we dug up above? Use those metrics to adjust your number upward or downward. They go on to say:

“As a general rule, small businesses with revenues less than $5 million should allocate 7–8 percent of their revenues to marketing. This budget should be split between 1) brand development costs (which includes all the channels you use to promote your brand, such as your website, blogs, sales collateral, etc.), and 2) the costs of promoting your business (campaigns, advertising, events, etc.). This percentage also assumes you have margins in the range of 10–12 percent (after you’ve covered your other expenses, including marketing).”

OK, so the SBA is telling us a range of 2–3% if we’re established and as high as 7–8% for those with revenue less than $5 million. Since the SBA might not exactly be keeping their finger on the pulse of the true “startup” scene, we should also consider another data point.

In his post, Ideal Ratio of Product Vs Marketing Spend for a Consumer Startup, GrowthHackers CEO Sean Ellis talks about when to make the adjustment of funneling more cash into marketing. He suggests a 95/5 ratio between product and marketing initially during product development. Once you’ve validated that people want or need your product, the spend ratio tips heavily towards marketing, with some companies spending as much 80% on marketing and 20% on product.

As with anything, it’s hard to throw out a magical number for your marketing spend. However, I could say it’s important to determine the average lifetime value of your customer and then figure out the cost to acquire them. If you can get things dialed into where you’re getting greater than a dollar in return for every dollar you spend on advertising/marketing, then you should scale up those initiatives as high as you possibly can.

Closing a Sale

Most people think they’re good at sales but actually suck at it. They say “sales is easy, anyone can do it.” But the reality is, convincing people to do something (e.g., buy your product, fund your company, join your team) is one of the hardest things in life.

Think about it. People are lazy and like to stick with what they’ve got. In addition, you might be in a market like we are (hosting) where there is lots of competition. If there are ten players in your space, statistically you’ve only got a 10% chance of getting someone’s business.

The Best Sales Book Ever

Robert Cialdini wrote Influence: The Psychology of Persuasion in 1984. This was before anyone knew what a CRM, or even the internet, was. It has sold over two million copies and Fortune called it one of the 75 smartest business books of all time. When Harvard Business Review interviewed him, they wondered if he gave away too much information on how to hack the human brain.

So, yeah, this book is legit and worth reading. It talks about six key principles of influence and here I’ll relate each of those to sales.

Reciprocity

The human brain is wired to return favors. Humans hate to feel indebted to others. Ever wonder why it seems Macy’s has a sale every other week, why companies do free trials, or why companies spend all that time creating whitepapers and infographics? They’re giving you something to get something in return: your business.

One great way to incorporate this into your business is to be helpful to your community. If you’re in WordPress, answer questions on Quora or in forums and become known as a great resource. If you’ve answered a question for someone and they’re thinking about using your services, they’ll be more likely to pick you over someone who wasn’t willing to offer advice for free.

Commitment

If you’ve seen The Wolf of Wall Street or Boiler Room, then you probably remember how most of the stockbrokers opened up their pitch. They’d say something like “How about I start you off with a small investment, just 50 shares and we’ll see how things go.” That was their way of getting a small form of commitment, which makes it much easier to get larger investments later on.

Both of those movies were about scamming people so I’m not advocating that, but you get the idea. Another example would be the way many companies push hard to get you to “commit” to a demo or webinar of their product. They know this will increase the likelihood that you think of yourself as a customer and, hence, will be more likely to end up one.

Social Proof

This is one of the most used by web startups. Most human beings feel validated based on what others are doing. In other words, safety in numbers; humans like to do what we see other people doing.

So how are web startups using this? Visit the homepage of any tech startup and you’ll typically see a section allocated for logos of prominent clients. That’s because they understand the value of social proof. If they show 50 of the Fortune 100 companies on there, they know customers will think “Gosh, if they’re all using XYZ, maybe I should too.”

Authority

Another principle deals with authority and obedience. Sounds strange, but let me explain. Psychologists have done experiments where they have figures of authority ask people to do objectionable things and, more often than not, they do them, even if they know they are objectionable.

Titles and uniforms are some of the best ways to convey authority. Why do you think dentists like to be called “doctor” so much? It conveys greater authority. We’re taught as kids…“You’d better listen to your doctor,” and so forth. If the “doctor” says you need a $5,000 root canal, your response will probably be “Where do I sign?” even if you don’t need one.

What is the best way to take advantage of this? Having a prominent spokesperson is a great example. Starbucks hired Oprah to create and endorse one of their teas. Oprah did her “favorite things” list, which everyone loved, so she must know a great tea, right? When LegalZoom first started out they used Robert Shapiro’s face on their homepage and in their ads. Brilliant. People thought to themselves “Hey, a prominent lawyer founded this, so their services are good enough for me.”

Likability

People are more likely to be persuaded by people they like. One way this is used in the startup world is the “About Us” page. If you view a company’s “About Us” page and like the people you see and the way they carry themselves, then you’re more likely to buy from them.

CEOs are another example. If a CEO is well-liked, then their company will have an easier time converting customers. Part of the reason people buy Teslas is because Elon Musk is a modern day Tony Stark. He’s controversial, but people love (or love to hate) him.

Scarcity

Perceived scarcity leads to increased demand. Ever wonder why every other commercial says “limited time only” or something along those lines? It’s because they’re using this principle.

Flash sales sites are a great example of this. They force you to sign up with an email address to “get access to limited quantity deals” and then have a countdown showing the quantity remaining. Visitors think to themselves, “I’d better get that pair of shoes before it sells out” and, bam, another sale is made.

The Art of the WordPress Startup

Building a WordPress startup from the ground up takes more than just a bright idea, as I’ve covered here.

Perhaps the most well-received blog series we have ever published, we’ve condensed the entire series into this one master post. There’s also a digital download available where you can get all 20 chapters covered in the blog series, plus bonus features including forwards by WordPress community notables Chris Lema, Syed Balkhi, and Matt Medeiros. Also, we’ve included four short essays I’ve written. Let us know in the comments if you’d like a copy, and we’ll email it to you!

Whether you’re just starting out, or already on your way to success, these are my tips, advice, and guidance to help you on your way.